Barcelona, 5 de febrero del 2019.- Next we publish the full study of Deolitte: “Driving automotive supplier performance and growth in a slowing market” (2019).

After nearly a decade of unprecedented growth, the automotive industry may soon encounter a plateau. As disruption in the industry unfolds, automotive suppliers must develop innovative growth strategies to thrive in a completely new environment. There will be significant challenges ahead as traditional revenues for suppliers are at risk; however, there are also new opportunities that may significantly outweigh the risks that suppliers can take advantage of during this growth slowdown.

What do top-performing automotive suppliers have in common?

To explore what actions have resulted in superior performance and enterprise value creation, Deloitte Consulting LLP (Deloitte) has conducted its third Global Automotive Supplier Study that investigates the following:

• Forces that could significantly disrupt the automotive industry in the near and long term.

• Four potential future states and potential implications for automotive suppliers.

• New competitors, risks, and opportunities across automotive supply segments.

• Strategic choices suppliers should consider as they play to win.

What drives shareholder value?

Three key winning themes drove 90 percent of shareholder value (SHV) creation over the past decade:

• Cost and asset efficiency: Focused on cost, improved profitability, and cash flow through restructuring and right-sizing facilities and operations.

• Product portfolio leadership: Shed commodity assets and focused portfolio to pursue growing product segments.

• Market-focused innovation: Invested in organic and inorganic growth in innovation in growing product segments.

There will be significant challenges ahead as traditional revenues for suppliers are at risk; however, there are also new opportunities that may significantly outweigh the risks that suppliers can take advantage of during this growth slowdown.

Stellar past performance does not guarantee the same for future performance

The composition of the top one-third of performers significantly changed over

the last five years compared to that of the previous five years. Of the 41 companies in the top one-third category from prior Global Automotive Supplier Studies, only three of those companies are still in the top one- third from 2012 to 2016. Interestingly, those three companies spent twice the amount on research and development (R&D) as a percentage of revenue than those who did not remain at the top. Those companies

are also much more “asset light,” averaging higher return on assets (ROA).

Disruptive innovation changing the game

The automotive industry is at the cusp of undergoing major transformation, and three key forces could cause disruption in the near and long-term future.

- Volume headwinds: In the near term, several original equipment manufacturers (OEMs) forecast lower global demand, and growth is expected to plateau in most markets. Volume headwinds may persist over the long term as a result of shared mobility, autonomous vehicles, etc.

- Traditional value chain is under attack: New, untraditional players now operating in the automotive industry have added in an unexpected layer of competition to the fold, changing industry dynamics. Move over, these new players are disrupting the traditional linear value chain by leapfrogging tiers, forming multitiered partnerships, etc.

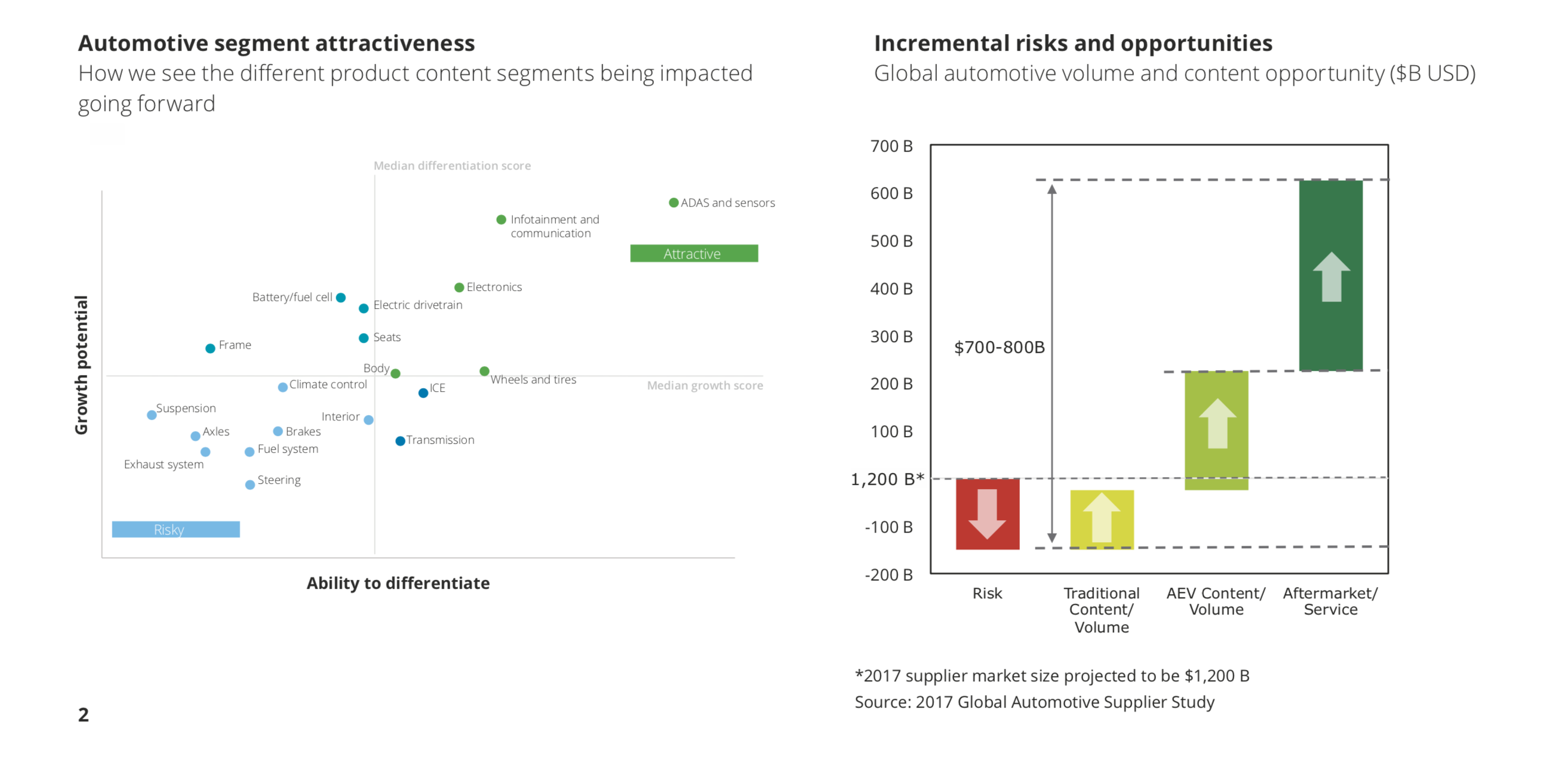

- Vehicle content and technology disruption: Certain segments are at risk of commoditization while others are more attractive for differentiation. Meanwhile, value creation opportunities are expected to shift to data- and service-driven offerings.

What does the future look like for automotive suppliers?

The Deloitte study outlines four possible scenarios that could occur in the next 10 to 15 years.

Scenario 1, Drag on: The industry is not so disrupted after all. While disruptive trends continue to be a hot topic at conferences, they fail to take a meaningful share of the market. Companies continue to position for future innovation and deliver great returns to investors.

Scenario 2, Repositioned: Disruption happens. Cars are transformed and new technologies capture the millennial market, offsetting the volume declines from disruption. Companies in turn adapt to these new business ecosystems and grasp at new opportunities.

Scenario 3, Downturn: The macro-economy stalls and commodity prices rise. Disruptive trends fail to materialize in medium term and the market is not impacted. Companies go back to batten down the hatches and look for roll-up opportunities.

Scenario 4, Disruption pressure: Shared driving makes a large dent in car volume and the future car is significantly different than the car of today—highly connected, shared, and autonomous. Certain segments are under significant pressure; however, at the same time, new opportunities abound.

The composition of the top one-third of performers significantly changed over the last five years compared to that of the previous five years. Of the 41 companies in the top one-third category from prior Global Automotive Supplier Studies, only three of those companies are still in the top one-third from 2012–2016.

You must be logged in to post a comment.